The National Warehouse Pricing Index rises for the first time in 13 months, signaling potential capacity constraints in port markets from front loaded inventories.

Demand for bonded and FTZ warehouse space explodes; with search traffic increasing 150+% in the last 3 months.

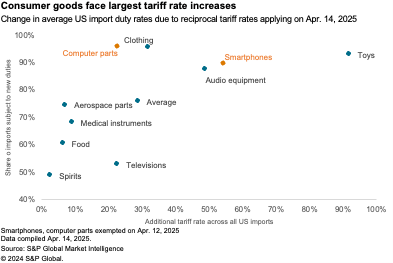

Toys, audio equipment, and apparel products are expected to be the most impacted by changes in tariffs, with average increases being 92%, 49%, and 32% higher, respectively, than in 2024.

The Warehouse Pricing Index (WPI) is available in the Journal of Commerce’s extensive, multi-channel dashboard, Gateway. Learn more about Gateway and how WarehouseQuote is helping logistics managers make smart supply chain decisions.

U.S. Warehousing Market Watch

7.0% National Industrial Vacancy Rate

111.6 National Warehouse Pricing Index Reading

The Demand for Customs Bonded and FTZ Warehouse Space Amid Tariff Concerns

Search traffic for bonded and Foreign Trade Zone (FTZ) warehousing has increased by an average of 150+% over the past three months compared to last year. This surge in demand is closely linked to Trump’s tariff plan, as importers are seeking a “safe harbor” for their inventory amid the shifting foreign policy landscape. In an environment of rising tariffs, companies may utilize these types of warehouses for several strategic purposes:

Delay duty payments to better manage cash flow.

Avoid duties entirely on goods that are re-exported.

Pay lower duties when the rate on components is less than that of the finished product.

Store inventory while waiting for favorable market conditions or changes in tariff policies.

Customs Bonded and FTZ warehouses can be valuable tools for companies to navigate the complexities and costs associated with increased tariffs.

Tariff Advisory: What to Consider Before Transitioning Inventory into a Bonded Warehouse

Customs Bonded Warehouses and Foreign Trade Zones (FTZs) offer significant cash flow advantages for importers. They allow companies to defer duty payments, enabling them to wait for more favorable market conditions. With the rise in tariffs, the benefit of delaying duty payments can result in significant cash flow savings as duties are only paid when the goods are distributed in the U.S. For businesses that depend on imported goods, utilizing these options is often the correct decision.

However, this flexibility comes with a cost; these facilities usually charge a premium compared to standard warehouses due to increased security, compliance, and bonding requirements. WarehouseQuote sees rates ranging anywhere from 1.5 to 4 times more than a traditional warehouse. Understanding this trade-off is necessary for making the right decision for your supply chain strategy.

Making the right choice requires weighing specific operational and strategic factors. In summary, it’s important to note the following when exploring customs bonded warehouse options:

Shippers can store product for up to five years, buffer against uncertainty, or wait to for changes in market conditions (i.e. lower tariff duties)

Bonded warehouse rates can range from 1.5-4x more than a traditional warehouse

There is a limited amount of U.S. bonded warehouse space available

Utilize Foreign Trade Zones to Lower Tariff Duties

While both Customs Bonded and FTZ Warehouses offer similar benefits when it comes to duty deferment, there are a few key differences that might make an FTZ warehouse more attractive than a customs bonded option.

Foreign Trade Zones, or FTZ’s, are geographical areas within the U.S. that receive the same Customs treatment as goods that are outside of the U.S. companies are able to use this area for storing, manipulating, manufacturing, or disposing of goods to then either export, or distribute into the U.S. under a more favorable tariff.

An example of an effective use of this space comes from the technology industry, where manufacturers can import the hundreds of components used to make a phone or laptop and assemble them in an FTZ. By distributing the final product to the US they are only paying tariffs on the finished product, as opposed to the hundreds of individual pieces that made the product.

Key Differences between FTZ and Customs Bonded Facilities

Customs bonded spaces hold goods within the U.S. on bond, meaning a percentage of the potential tariff is held by Customs Agents. In contrast, goods held in FTZ space are considered outside of the US.

Goods can only be stored for a set amount of time (typically 5 years) in Customs Bonded spaces, whereas goods can remain indefinitely in FTZ spaces.

Most customs bonded warehouses only allow for certain manipulations like cleaning, repacking, and sorting. FTZ spaces are more flexible, allowing manufacturing, assembly, processing, testing, and other activities.

The paperwork and entry procedures typically are more cumbersome for Customs Bonded space, as the goods are admitted through customs into the US. FTZ spaces allow for more flexibility on re-export and require less documentation on entry.

While customs bonded and FTZ warehouses offer valuable cash flow advantages and duty deferral, businesses must carefully weigh the increased operational costs and regulatory complexities. The decision to utilize these facilities should be driven by a strategic assessment of specific needs, considering the trade-off between financial benefits and operational constraints.

If your team is exploring customs bonded or FTZ warehousing options, please reach out to our team and we can help determine if it is a suitable solution for your business.

Tap Into WarehouseQuote’s Customs Bonded and FTZ Warehouse Network

Is your company exploring utilizing bonded and FTZ warehouses? WarehouseQuote has established relationships with 70+ warehouses throughout the US with Customs Bonded or FTZ designations.

National Warehouse Pricing Index

The National Warehouse Pricing Index (WPI) increased 0.3 percent month-over-month (MOM), marking the first increase in 13 months. The combination of shippers front loading inventory, labor costs, and annual rate increases are likely contributors to increase in services.

Regional Warehouse Pricing Index

All U.S. regions have seen a pricing decrease year-over-year for warehousing services. The Midwest saw a marginal increase at 0.3 percent, followed by declines in the Northeast, South, West regions at -1.4 percent, -3.0 percent, and -4.3 percent, respectively.

The Voice of WarehouseQuote

“Due to the extreme volatility in the Bonded and Foreign Trade Zone markets, XoLogistic is advising clients to remain cautious. Tariff implications are creating significant uncertainty, and many businesses are concerned about how these shifts will impact their operations and profit margins. Given the fluid nature of the current trade environment, we strongly recommend clients continue to monitor market trends closely and reassess strategies on a daily basis. In addition, we encourage a thorough review of all raw and sourced materials, specifically their points of origin. Identifying alternative manufacturing locations or sourcing options may reveal opportunities to reduce costs and maintain margin stability in the face of shifting tariff structures.” – James Paquette, Head of Logistics Operations at XoLogistic

A Very Different Peak Season: Seasonal Supply Chain Strategies in the Face of Tariffs

Chris Rogers Head of Supply Chain Research, S&P Global Market Intelligence

Every peak season – covering deliveries into North America and Europe for the back-to-school and winter holiday shopping periods – brings a different set of challenges, whether it’s the pandemic demand uncertainties of 2020 and 2021, inventory rebalancing in 2022, the Panama Canal disruptions in 2023 or the risk of US port strikes in 2024.

In 2025 of course the main challenge is calling the timing of US-inbound shipments relative to the uncertainties of import duties applied by the administration of President Donald J. Trump. The “reciprocal” tariffs applied against all countries at a rate of 10% and against mainland China of 125% (plus 20% applied under an earlier program) are already in place but could climb rapidly in early July if trade deals are not reached.

Consumer goods where imports from mainland China are particularly important face the highest tariffs. S&P Global Market Intelligence estimates indicate import duties on average for toys are 91.8% points higher than in 2024, while audio equipment face duties that are 48.8% points higher and apparel 31.9% higher.

Even imports from free trade partners Mexico and Canada are under tariff uncertainties due to the temporary absence of tariffs for USMCA-compliant products and the prospect of a renegotiation of the trade agreement following Canada’s elections.

Aside from country-specific tariffs there’s nine separate product-level tariff programs and investigations ranging from trucks and cars to critical minerals and copper which bring further tariff risks with uncertain timing. The most important of these is a review of the electronics sector including key seasonal devices such as smartphones and laptop computers where tariffs could be applied as soon as late May or as late as January 2026, or not at all.

The good news is that firms have a wide range of potential tactical and strategic options for dealing with the economic and organizational impact of tariffs heading into the peak shipping season.

The most likely route to be followed by most companies, as evidenced by earnings conference calls held over the past three months, is to increase at least part of the cost of tariffs through to customers. With retail margins typically around 50% of the final price, products that are heavily dependent on imports could see double-digit percentage price rises.

A second, related route is to share the burden of tariffs with suppliers. While the actual payment of duties is the responsibility of the importer, many firms have indicated they are approaching suppliers to obtain discounts to offset part of the tariffs. This has received pushback in some instances, including from national governments.

In a related, forward-looking strategy, procurement managers are increasingly treating tariffs as a separate cost-pass through line item in a similar approach to that used for commodity costs and shipping expenses.

A key challenge for imports from mainland China is the high level of import duty bond payments required as every US$100 of imports requires US$140 of tariff payments. That’s leading to an increased use of free trade zones and requests for bonded warehouses to more closely stage the payment of duties to the final sale of products at the retail level for cash flow management purposes.

The reshoring of purchases – ie buying from countries that have or may in the future have lower tariff rates – can work on a tactical level as well as a strategic level. This can introduce single-supplier risk but mitigates cash costs in the near term.

In the long-term, firms will likely continue to process of diversifying sourcing though investment decisions are being put on hold until there’s more certainty on tariffs – a process that is likely to take well beyond the 2025 peak season decision making period.

Tariffs and Truckload Tensions: Navigating the Freight Fallout of Trade Policy in 2025

Mathew Leo Principal Manager, Research and Market Intelligence, C.H. Robinson

As the freight industry heads into spring 2025, U.S. trade policy is emerging as one of the most influential forces shaping North American supply chains. The sweeping U.S. tariff announcements released on April 2nd marked a turning point, instituting the broadest tariff increase in modern U.S. history, imposing a baseline 10% on all imports. While some of the other country specific tariffs are currently paused, additional tariffs to trade with China as well as other industry specific commodities have created a complex environment for shippers.

The immediate effect has been a flurry of activity among importers to pull shipments forward to get ahead of tariff implementation. This surge in inbound volumes, especially from Asia, has intensified near-term truckload demand at ports and inland distribution hubs. However, this demand spike may be short-lived as some shippers pause due to tariff uncertainties.

Strategic Warehousing amid Tariff Uncertainty

This pull-forward of inventory resulted in a spike in demand for warehouse space, especially near ports and distribution hubs. Now with additional tariffs potentially looming, some shippers may be looking to continue this pull-forward before industry-specific tariffs are implemented. Since some see a portion of the tariffs being a negotiation tactic, there has been some sentiment that tariffs could calm down in the coming months. Whether they do or not, the uncertainty has driven more and more shippers to look into bonded warehousing options. These facilities allow imported goods to be stored under customs control, enabling businesses to defer duty payments. The hopes are that this would allow these shippers to potentially time the release of these goods more strategically if tariffs are reduced later.

Nearshoring Growing More Attractive?

Aside from the goal of driving more sourcing of manufacturing and goods domestically, there is another potential for a renewed push toward nearshoring. Some U.S. companies are actively exploring how to reduce exposure to volatile overseas trade relationships and move manufacturing closer to end markets. Mexico, already a top trading partner, is at the forefront of those conversations, particularly in the automotive industry.

Nearshoring does not come without its own challenges and tariff uncertainties. Tariffs exist and the future of those are still in flux, as well as retaliatory tariffs. There is an exemption for goods that qualify for the USMCA, which has resulted in a surge of shippers looking to shore up that paperwork to avoid the 25% tariffs.

This also changes the warehousing landscape. For example, facilities along the U.S.–Mexico border could continue to see stress as shippers look to increase freight demand northbound.

Strategies for Shippers

In this fluid environment, shippers are advised to adopt more agile and data-driven supply chain strategies. This includes:

Impact analysis: Assess how tariff scenarios could impact landed cost and margin.

Customs preparedness: Gathering documentation on their products’ country of origin, the origin of steel or aluminum content in their products, and other newly required details

Bond review: Assessing the adequacy of their company’s customs bond, which guarantees to U.S. Customs and Border Protection that you’re able to pay the duties you owe.

USMCA strategy: Seeking to qualify their products under the U.S.-Mexico-Canada Free Trade Agreement in order to avoid the 25% U.S. tariff on goods from Canada and Mexico.

The LMI score is a combination of eight unique components that make up the logistics industry, including: inventory levels and costs, warehousing capacity, utilization, and prices, and transportation capacity, utilization, and prices. The LMI is calculated using a diffusion index, in which any reading above 50.0 indicates that logistics is expanding; a reading below 50.0 is indicative of a shrinking logistics industry.

Industrial Real Estate Vacancy Rates

Industrial real estate vacancy rate is the percentage of available industrial property, such as a warehouse or distribution center.

United States Regional Divisions

Midwest

East North Central: Illinois, Indiana, Michigan, Ohio, and Wisconsin

West North Central: Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, and South Dakota

Northeast

New England: Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont

Middle Atlantic: New Jersey, New York, Pennsylvania

South

South Atlantic: Delaware, Florida, Georgia, Maryland, North Carolina, South Carolina, Virginia, Washington DC, and West Virginia

East South Central: Alabama, Kentucky, Mississippi, and Tennessee

West South Central: Arkansas, Louisiana, Oklahoma, and Texas

WarehouseQuote’s Economic Commentary Disclaimer

The material and content used in this publication is for informational purposes only. Reference to any third party (including external hyperlinks) does not constitute or imply the endorsement of said third party. WarehouseQuote does not warrant the accuracy or completeness of the Content. The views and opinions expressed herein are those of the author and do not necessarily reflect the official policy or position of WarehouseQuote. Reproduction of the Content may be made only with the written permission from WarehouseQuote.

Chris Rogers Head of Supply Chain Research, S&P Global Market Intelligence

Mathew Leo Principal Manager, Research and Market Intelligence, C.H. Robinson

About WarehouseQuote

WarehouseQuote is a managed warehousing solution helping middle market and enterprise businesses scale their warehouse operations with precision. Through our 3PL warehousing and fulfillment network of 250+ facilities, integrated technology platform, and in-house supply chain expertise, we enable businesses to design efficient fulfillment networks connected by a single technology platform. Hundreds of B2B and B2C businesses like Chatime, Joyride, Benitago Group, Big Ass Fans, and Mighty Good Solutions use WarehouseQuote to scale, streamline, and optimize their warehouse operations.